By Marat Iliyasov

Ramzan Kadyrov, Kremlin-backed Chechen leader, faces serious allegations. A German NGO, the European Centre for Constitutional and Human Rights, accuses him of leading LGBTQ+ purges in Chechnya; Georgia alleged that he plotted journalist Giorgi Gabunia’s murder; while Ukraine accuses his forces of committing war crimes. Reports also link him to kidnappings, torture, and the murder of Chechen opposition figures and bloggers across Europe and Turkey. These accusations could place Kadyrov alongside internationally tried criminals such as former president of Serbia Slobodan Milošević or the Deputy Führer of the Nazi Party Rudolf Hess. But…, is this scenario plausible?

Photo source: tatarstan.ru

BACKGROUND: To begin with, it is important to examine how the International Criminal Court (ICC) and ad hoc tribunals are formed, who can submit a case to the ICC, and which individuals can be indicted.

The establishment of international tribunals and ICC are rooted in international law and the broader aim of creating a more just and accountable world. This development began after WWII, when military and political leaders from Nazi Germany and Imperial Japan were tried for their war crimes. These tribunals set a crucial precedent purported to halt crimes against humanity that concern the international community.

The Cold War (1946-1991) between the US and the USSR severely curtailed the enforcement of international justice. Crimes committed during this era often went unpunished because the perpetrators had the backing of these superpowers, which could effectively obstruct investigations or prosecutions via the UN Security Council. Without the willingness and cooperation of world powers and the countries involved, tribunals either could not be created or lacked enforcement mechanisms. For example, it took decades to try the Khmer Rouge’s crimes committed in 1970s in Cambodia. It became possible only when the Cambodian government finally supported the idea of establishing the Extraordinary Chambers in the Court of Cambodia (ECCC).

The fall of Communism in 1991 triggered more international armed conflicts and consequently war crimes. It also created new opportunities for international justice. The tribunals for former Yugoslavia, Rwanda, and Sierra Leone strengthened the possibility of prosecuting high-ranking officials for crimes against humanity. Notably, these courts succeeded in convicting former Serbia's President Slobodan Milošević and former Liberian President Charles Taylor—figures once deemed untouchable. These trials, same as the tribunals for Rwanda, Yugoslavia, and Liberia were made possible by key shifts in the internal power structures of these countries.

Even today, the willingness and collaboration of the domestic power structures remain the most important element in determining the feasibility of initiating a case. To prosecute Kadyrov, such cooperation would be required from Russia, which has consistently demonstrated its unwillingness to collaborate with the international bodies. Therefore, building a case against Kadyrov could potentially achieve only limited success, similar to the international tribunal for Lebanon. Established in 2009 to prosecute Hezbollah members for the assassination of Lebanon's Prime Minister Rafic Hariri in 2005, this special tribunal convicted and sentenced the identified culprits in absentia. This means that they can be punished only if captured, which renders this trial largely symbolic.

IMPLICATIONS: Various actors could theoretically initiate proceedings against Kadyrov, including the United Nations Security Council (UNSC), prosecutors from the International Criminal Court (ICC), national governments appealing for UN intervention, international organizations such as Amnesty International, and supreme courts of foreign countries invoking the principle of universal jurisdiction to prosecute war criminals.

However, the likelihood of any of these actors successfully leading such an initiative against Kadyrov and bringing him to justice remains low. The UNSC could act only if Russia, as a permanent member of the Council, either refrains from using its veto or initiates the process itself—both of which are highly unlikely. Russia has a long history of misusing its veto power in the UNSC and is a country where the rule of law is frequently breached. Moreover, given Kadyrov’s strong ties to Russian President Vladimir Putin, it is nearly inconceivable that Russia would support or initiate such efforts.

Initiatives could also come from international organizations, the ICC, national governments, or national courts of foreign countries under the principle of universal jurisdiction. To build a case, these initiators must gather substantial evidence and secure the cooperation of experts and witnesses. The ICC’s 2023 indictment of Vladimir Putin for war crimes demonstrates the institution's willingness to take bold action, such as cases initiated by Ukraine for war crimes committed on its territory by the Russian military. However, this does not guarantee that Kadyrov will be brought to court. The ICC's arrest warrant for Putin demonstrates the limitations of international justice. The warrant has neither been enforced, nor has it prevented him from visiting countries where he should have been arrested.

Another question to consider is: what crimes could Kadyrov be prosecuted for? He has long been accused of systematically violating human rights in Chechnya and beyond. Journalistic investigations and witness testimonies suggest that he has personally overseen or ordered acts of torture, extrajudicial killings, the persecution of LGBTQ+ individuals (including the execution of dozens during an alleged "purification" campaign), enforced disappearances, and repression of dissent. If substantial evidence—including testimonies, forensic analyses, and classified documents—supports these claims, he could be directly prosecuted.

However, gathering such proof would be extremely difficult. Despite the existence of survivors and witnesses, most would be reluctant to testify due to fears of retaliation against themselves or their family members still living in Chechnya. Given that witness protection programs in the EU and the US do not cover the relatives of witnesses, it is hard to imagine any foreign government taking the risk of extracting multiple family members from Chechnya, resettling them elsewhere, and supporting them financially. Without such assurances, convincing people to testify against Kadyrov and prove his involvement in these crimes would be an immense challenge.

Another set of crimes Kadyrov could potentially be tried for are war crimes in Ukraine. Since Russia's 2022 invasion of Ukraine, Kadyrov’s forces—known as the Kadyrovtsy—have faced multiple accusations of violating the rules and regulations of international humanitarian law, known as jus in bello. These allegations could support the building of a case against Kadyrov under the principle of command responsibility. However, given difficulties of documenting of documenting crimes during wartime, it is unlikely that sufficient evidence implicating Kadyrov in issuing direct orders to commit war crimes will ever be found.

Lastly, it is important to note that Kadyrov's troops are part of the broader Russian military. This means that any tribunal would need to address not only Kadyrov, but also the entire Russian military command and political leadership. This brings us back to the minimal likelihood of such a scenario, given the strong political resistance from the Russian leadership against international justice.

CONCLUSION: Establishing an international tribunal against Kadyrov faces considerable legal, technical, and political obstacles. The biggest of these is the lack of willingness and cooperation from the Russian leadership, which shields Kadyrov from legal consequences both domestically and internationally. The likelihood of Russian collaboration, even if international bodies were to initiate a case against Kadyrov, is minimal. This is largely because Kadyrov’s case cannot be investigated in isolation from the Russian political leadership. Therefore, creating an international tribunal for Kadyrov is a highly unlikely scenario. It cannot happen without a significant overhaul of Russia's power structures, as historical examples of successful international tribunals demonstrate.

AUTHOR BIO: Marat Iliyasov is a Visiting Assistant Professor at the College of the Holy Cross. His focus is post-Soviet politics and conflicts in wider Eurasia.

By Mehmet Fatih Oztarsu

The first EU–Central Asia Summit took place amid intensifying global competition, emphasizing the EU’s efforts to strengthen ties through connectivity, economic diversification and access to critical raw materials. Key regional concerns—including migration, sanctions circumvention, and infrastructure gaps—were also addressed. There is growing anticipation that the EU will adopt a more holistic and regionally attuned strategy, moving beyond great power rivalry to foster inclusive, long-term partnerships. Such an approach would bolster the EU’s credibility as a constructive and complementary actor in Central Asia’s evolving geopolitical landscape. Instead of competing against Russia and China, the EU can play more effective role as a reliable partner.

Photo source: Framalicious

BACKGROUND: The first EU–Central Asia Summit was held in Uzbekistan on April 4, 2025, in Uzbekistan. The EU was represented by President of the European Council António Costa and Head of the European Commission Ursula von der Leyen. During the summit, multilateral relations were addressed in a comprehensive and multidimensional manner. The parties discussed various areas of cooperation, including security challenges, economic collaboration, connectivity under the Global Gateway framework and people-to-people ties.

The EU holds a distinct position in the region, being Central Asia’s second-largest trading partner and its largest investor, accounting for 22.6 percent of the region’s foreign trade and 40 percent of foreign investments. In particular, Kyrgyzstan, Uzbekistan and Tajikistan have expressed their intention to further develop trade relations with Europe under the Generalised Scheme of Preferences (GSP), which facilitates more favorable access to the EU market.

This summit is also significant given its timing—coinciding with a period in which the U.S., alongside Russia and China, has emerged as a competitor to the EU in the region. In this new geopolitical landscape, strengthening relations with alternative markets has become a strategic objective for all major actors. However, the EU is expected to adopt a clearer stance on key issues in its evolving engagement with Central Asia. There are growing expectations that the EU will address the unintended negative impacts of its sanctions on Russia, which have also affected the region. Additionally, greater emphasis is expected on areas that align more closely with the region’s pressing needs—such as agricultural development and connectivity infrastructure—rather than focusing narrowly on selected industries or geopolitical competition.

IMPLICATIONS: The EU’s timely convening of the Central Asia Summit coincided with a period in which global developments are compelling all countries to make new strategic choices. Actors affected by the protectionist U.S. economic policies, Russia’s war in Ukraine, and China’s rapid and seemingly unstoppable economic expansion are increasingly seeking new avenues for cooperation. While the EU already maintains a satisfactory level of economic engagement with the region, this new initiative signals an ambition to address more niche and forward-looking areas. These include specific areas such as geographical and digital connectivity, the green economy, critical raw materials and water management.

Within the Global Gateway initiative, the EU has sought to engage with the region primarily through infrastructure projects, allocating a budget of €300 million for this purpose. Although the EU’s initial intention was, to some extent, to compete with China, it has opted for a more nuanced and tempered approach in recent years. As Dr. Stefan Meister from the German Council on Foreign Relations explains, “EU is not about seriously challenging China and Russia, but rather about offering some alternatives in some sectors, competing in some sectors—especially on raw materials and on connectivity.” This perspective reflects the EU’s new approach of pragmatic engagement rather than direct confrontation, seeking to expand its influence through sector-specific cooperation and strategic investments.

Given China’s geographical proximity and economic leverage, it has become clear that directly confronting Beijing’s dominant position in Central Asia would yield little benefit for any actor involved. Instead, the EU has pursued a strategy of complementarity rather than rivalry. Central Asian countries, positioned to benefit from this geopolitical pragmatism, stand to gain significantly—particularly through the further development of the Trans-Caspian Transport Corridor, which promises to enhance regional connectivity, linking the EU and Central Asia within 15 days and expanding their access to diversified markets.

In addition, the issue of critical minerals is also of great importance in the new period. The EU’s Critical Raw Materials Act, proposed in March 2023, aims to ensure a secure, sustainable and diversified supply of critical raw materials essential for strategic sectors. As demand for materials like rare earths and especially lithium is projected to increase up to twelvefold by 2030, the EU seeks to reduce its overreliance on single third-country suppliers. The Act sets specific targets: at least 10 percent of the EU’s annual consumption should be extracted within Europe, 40 percent processed, and 25 percent recycled, with no more than 65 percent of any strategic raw material imported from a single external source. These measures are central to the EU’s efforts to diverse partnerships with Central Asia.

Kazakhstan’s substantial uranium reserves and its role as a producer of 19 critical raw materials essential to the EU make it a strategically important partner. Additionally, Kyrgyzstan, Tajikistan, and Uzbekistan possess reserves of 43, 17, and 71 critical minerals respectively, further enhancing the region’s value from the EU’s perspective. However, despite this resource richness, the region’s transport connectivity remains heavily influenced by Russia and China—posing a significant challenge for the EU as it seeks to establish independent and secure supply routes.

Migration constitutes a growing challenge in EU–Central Asia relations in addition to the risk of sanctions circumvention and agriculture development limitations. The EU has expressed increasing concern over migration flows originating from or transiting through the region—particularly given instability in Afghanistan and broader socioeconomic pressures within Central Asia. Despite this pragmatic exchange, questions remain about the long-term sustainability and oversight of such processes.

On the other hand, an increasing number of Russian companies are reportedly using Central Asia to circumvent Western sanctions, raising concern within the EU. Russian-affiliated businessmen have begun relocating portions of their assets to countries in the region to shield them from asset freezes, a development the EU views unfavorably. In 2024, several companies were added to the U.S. sanctions list. Additionally, remittances from Russia remain a vital source of income for countries like Tajikistan and Kyrgyzstan. However, since the imposition of sanctions, this financial flow has become unstable, posing significant challenges to the economic stability of these remittance-dependent economies. The EU needs to address this issue in the future since there is no specifically designed policy to resolve it.

Lastly, the EU has been slow to support the broader economic development of Central Asia. According to World Bank data, the agriculture sector remains a weak component of total GDP in the region: 4 percent in Kazakhstan, 9 percent in Kyrgyzstan, 11 percent in Turkmenistan, 20 percent in Uzbekistan and 22 percent in Tajikistan. The service sector dominates these economies, accounting for 56 percent in Kazakhstan, 52 percent in Kyrgyzstan, 45 percent in Turkmenistan, 43 percent in Uzbekistan, and 35 percent in Tajikistan. Under these conditions, the EU needs to play an effective role in strengthening the region’s capacity for industrial production and economic diversification. A narrowly focused strategy centered solely on gas, oil, and critical raw materials risks undermining the long-term goals of sustainable and inclusive cooperation.

CONCLUSION: Although EU policy frameworks are often presented with ambitious and appealing labels, critical areas remain that require greater attention in Central Asia. Rather than pursuing selective economic cooperation, the EU should prioritize agricultural development, the diversification of industrial sectors and the provision of sufficient infrastructure support. Moreover, a clear and coherent stance on the indirect impact of sanctions against Russia in the region is urgently needed. These ongoing uncertainties and regional expectations will play a defining role in shaping the future trajectory of EU–Central Asia relations.

On the other hand, framing cooperation with Central Asia solely as a tool for competing with Russia and China is unlikely to yield meaningful benefits for either the EU or the region. A more constructive approach would involve the EU positioning itself as a complementary partner, offering alternatives rather than rivalry. This strategy not only fosters regional stability but also helps mitigate the negative effects of U.S. protectionist tendencies, thereby strengthening the EU’s credibility as a balanced and reliable actor in Central Asia.

AUTHOR BIO: Dr Mehmet Fatih Oztarsu is Assistant Professor at Joongbu University and Senior Researcher at the Institute of EU Studies at Hankuk University of Foreign Studies. He studied and worked in Baku, Yerevan, Tbilisi, and Seoul as an academic and journalist. He is the author of numerous articles and books on South Caucasus and Central Asian affairs.

By Michael Tanchum

The Eastern Mediterranean and the Black Sea are one natural waterway forming the core of a multi-modal connectivity arc that can serve as the transportation backbone of a commercial corridor spanning the Middle East and Central Asia. Azerbaijan’s inclusion in a wider Abraham Accords framework could radically reconfigure trade patterns and manufacturing value chains across the southern rim of Eurasia, to the benefit of U.S. strategic interests and those of its partners. While strengthening U.S.-Israel-Azerbaijan trilateral defense cooperation is a response to the looming prospect of a military showdown with Iran, the geo-economic significance of Azerbaijan’s inclusion in the Abraham Accords is of long-term strategic consequence. With the ports on Israel’s Eastern Mediterraneancoast and Azerbaijan’s Caspian Sea coast serving as anchor points, the India-Middle East-Europe Corridor can be linked to the Trans-Caspian International Transport Route, creating an crescent of commercial cooperation from India to the Central Asian Republics via the UAE, Saudi Arabia, Jordan, Israel, Georgia, and Azerbaijan, providing counterweight to the westward expansion of Chinese economic hegemony across the Central Asia-Caucasus region and the Middle East.

Photo source: Michael Tanchum

BACKGROUND: In early March 2025, the office of Israeli Prime Minister Binyamin Netanyahu made public that it favors elevating the trilateral partnership between Israel, Azerbaijan and the U.S.. Following a motion in the Israeli Knesset on "Upgrading the Strategic Alliance between Israel and Azerbaijan," a flurry of calls arose for Azerbaijan’s inclusion in the Abraham Accords. The September 15, 2020, agreement normalized relations between the United Arab Emirates (UAE) and Israel, followed by the establishment of relations between Israel and Bahrain and Sudan, respectively, and the restoration of relations with Morocco. The Abraham Accords also consists of an expanded framework of strategic and economic initiatives among the participants, developed in partnership with the U.S.

Azerbaijan and Israel have enjoyed an all-weather strategic relationship since diplomatic relations were established in the early 1990s following Azerbaijan’s independence. The two states have developed deep defense cooperation over the past 30 years, based on countering the threat Iran poses to both Israel and Azerbaijan, which shares a 428-mile (689 km) border with the Islamic Republic. Key proponents of extending the Abraham Accords to Azerbaijan have emphasized the Azerbaijani-Israeli defense relationship’s durability and Azerbaijan’s reliability as a principal oil supplier to Israel. Azerbaijan and Israel enjoy commercial cooperation in telecoms and other technology sectors. The State Oil Company of Azerbaijan (SOCAR) recently established the new subsidiary “SOCAR Tamar” following its March 17, 2025 acquisition of a 10 percent stake in Israel’s Tamar offshore natural gas field in the Eastern Mediterranean. Azerbaijan has also played an important mediating role between Baku’s close partner Turkey and Israel during times of tension.

Netanyahu’s public commitment to strengthen Israel’s trilateral relationship with Azerbaijan and the U.S was preceded by a collection of letters sent to U.S. President Donald Trump at the end of February by prominent rabbis advocating Azerbaijan’s inclusion in the Abraham Accords. Among them was a senior rabbi in the UAE and personal friend of Trump’s son-in-law Jared Kushner, who played a key role in the signing of the Abraham Accords. Additionally, opinion pieces from Israeli and American policy communities, including in the Wall Street Journal, added further political momentum amidst escalating tensions between Washington and Tehran over Iran’s nuclear weapons program. Two days after Iran’s Supreme Leader Ayatollah Ali Khamenei’s March 12, 2025, rejection of the U.S. proposal to hold negotiations about Tehran’s nuclear weapons program, Trump’s special envoy to the Middle East Steve Witkoff visited Baku after an overnight visit to Moscow, in what appears to be a coordinated effort to prepare for possible military action against Iran by Israel or the U.S., following the exhaustion of diplomatic efforts.

IMPLICATIONS: Beyond defense cooperation, a compelling strategic and geo-economic logic exists to include Azerbaijan in a wider Abraham Accords framework, building upon the Azerbaijan’s parallel and separate bilateral economic relations with Israel and the UAE. Extending the Abraham Accords framework outside the Arab World has precedence in the quadrilateral cooperation among India, Israel, the UAE, and the U.S. – the “I2U2” framework – emerging from India’s robust yet parallel commercial cooperation and joint venture investments with Israel and the UAE. Trilateral cooperation emerged organically from the synergies between India’s commercial ventures with Israel and the UAE, traditionally India’s third-largest trading partner and Arabian Sea neighbor.

In February 2022, the UAE signed a Comprehensive Economic Partnership Agreement (CEPA) with India followed by the May 2022 signing of a similar UAE-Israel free trade agreement. The two trade agreements paved the way for initiating three-way coordination in developing an India-Middle East Corridor. Quadrilateral cooperation involving the U.S. was then formalized with the July 2022 I2U2 summit.

The extended Abraham Accords cooperation gave rise to a vision of an India-to-Europe commercial corridor in which the UAE’s ports serve as the Indian Ocean connectivity node with Israel’s Eastern Mediterranean ports serving as the maritime outlet to Europe, connected by a UAE-to-Israel railway network transiting Saudi Arabia and Jordan. Once the transportation route is operational, Indian goods leaving Mumbai could arrive on the European mainland in as little as 10 days. An initiative to realize this corridor, now known as the India-Middle East-Europe Corridor (IMEC) was formalized with the signing of the September 9, 2023, Memorandum of Understanding at the New Delhi G20 Summit, with India, the U.S., the UAE, Saudi Arabia, France, Germany, Italy, and the EU as signatories.

Research has shown that commercial corridors only emerge where the requisite large investments in port and rail infrastructure are coupled with an industrial base anchored in manufacturing value chains. The IMEC is highly conducive for value chain integration because of the existing synergies between India’s commercial ventures with its Arab Gulf partners and its commercial ventures with Israel, as exemplified by the manufacturing value chain in food production that is one of the leading drivers of the IMEC’s development. India’s “Food Corridor to the Middle East” is driven by India’s investment partnerships with the UAE and Saudi Arabia that rely on the transformation of India’s agriculture and water management sectors being implemented through India’s partnership with Israel. Similar synergies exist in other sectors, with the most promising in green energy and innovative technology, which has already lead to joint venture production facilities in green manufacturing.

The inclusion of Azerbaijan, along with Georgia, in the wider Abraham Accords framework holds a similar potential to create a new trans-regional commercial architecture. The UAE is Azerbaijan’s top Arab trading partner, accounting for 40 percent of Azerbaijan’s trade with the Arab World. The UAE is also the largest Arab investor in Azerbaijan and one of the top 10 global investors in Azerbaijan, accounting for 7 percent of Azerbaijan’s FDI inflow. In 2023, the UAE’s Abu Dhabi National Oil Company acquired a 30 percent stake in Azerbaijan’s Absheron natural gas field in the Caspian Sea. Similarly, the UAE is Georgia’s largest trading partner in the Arab world, accounting for 63 percent of Georgia’s trade with the region. Trade is likely to increase further with the UAE-Georgia CEPA, which came into effect in June 2024. The UAE is also invested in solar power plant development in both Azerbaijan and Georgia. Most significantly, in March 2024, the UAE’s AD Ports group, acquired a 60 percent ownership share in the Tbilisi Dry Port, a new custom-bonded and rail-connected intermodal logistics hub in Georgia. At the heart of the Trans-Caspian Route, the port is a key logistics facility for the rail connection linking Georgia’s Black Sea coast and Azerbaijan’s Caspian coast.

Azerbaijan’s Baku port is the connectivity node from where the Wider Black Sea region connects to Central Asia across the Caspian Sea. The Trans-Caspian International Transport Route (TITR) connecting the Caspian and Black Seas via Azerbaijan and Georgia, commonly referred to as the Middle Corridor, was developed as an alternative to the Russia-based Northern Corridor for China-to-Europe trade. The TITR consists of multi-modal transportation links for container transshipment via Kazakhstan’s Caspian port Aktau to the specially constructed port of Baku at Alat from where goods can be shipped by railway connection from Azerbaijan to Georgia’s Black Sea ports and in turn to Israel’s Eastern Mediterranean ports. By linking IMEC and the TITR, India will possess its own multi-modal corridor to access Central Asia, enabling India to effectively compete with China in Eurasia without being reliant on Russia or Iran. IMEC provides India with a streamlined alternative to its 25-year effort to establish the troubled International North-South Transit Corridor (INSTC) to access Central Asia through Iran’s Chabahar port, serving as the Indian Ocean connectivity node with overland transportation links running northward via Iran and Afghanistan.

The multi-modal corridor connecting India to Central Asia would also open the opportunity for Turkey to participate in IMEC. The UAE’s ports and logistics giant DP World operates Turkey’s Yarımca port, reputed to be the most technologically advanced in Turkey. Yarımca’s Marmara coast location is highly suited for intermodal transportation in which cargo can be transshipped to the Black Sea or Georgia and Azerbaijan by rail from Kars via the Baku-Tbilisi-Kars railway.

CONCLUSION: The September 2023 signing of the IMEC declaration was preceded by the July 2022 I2U2 summit, the first convening of the heads of government of India, Israel, the UAE, and the U.S. As a step toward linking IMEC with the Trans-Caspian Corridor, a CC-I2U2 summit should be convened with the heads of Azerbaijan and Georgia participating. The format can be extended to include Central Asian Republics as well as Saudi Arabia and Jordan in anticipation of the extended arc of joint venture manufacturing investments and commercial cooperation.

By including Azerbaijan in a wider Abraham Accords framework, the U.S. can upend the geopolitics of connectivity in Central Asia, halting the westward expansion of Chinese commercial hegemony across the Eurasian landmass. Linking the IMEC corridor to the Caspian shores of Kazakhstan via a multi-modal sea route with trans-shipment across Georgia and Azerbaijan will effectively end India’s isolation from Central Asia – a strategic objective long sought by New Delhi. Consolidating the triangle of bilateral economic relationships among Azerbaijan, Israel, and the UAE into a multilateral framework through U.S. facilitation under the Abraham Accords is a necessary first step and a boon to the U.S. strategic position across Eurasia’s southern rim.

AUTHOR BIO: Prof. Michaël Tanchum teaches international relations of the Middle East and North Africa at the University of Navarra, Spain and an associate fellow in the Economics and Energy at the Middle East Institute in Washington, D.C. He is also a Senior Associate Fellow at the Austrian Institute for European and Security Studies (AIES) and an affiliated scholar of the Centre for Strategic Policy Implementation at Başkent University in Ankara, Turkey (Başkent-SAM) and the NTU-SBF Centre for African Studies in Singapore. @michaeltanchum

By Sergey Sukhankin

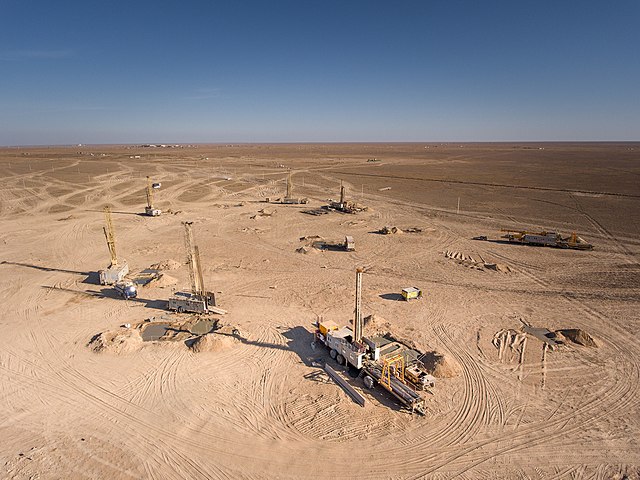

In early January 2025, operations at the uranium-producing Kazakhstan-based Joint Venture Inkai LLP (JV Inkai) were temporarily halted – the venture, established in the early 1990s, has been jointly managed by Kazatomprom (which holds a 60 percent stake) and the Canadian company Cameco (with 40 percent) – resulting in a brief decline in the share prices of both firms in New York and evident concern among Canadian investors. After a short interruption, activities at Inkai resumed without disruption. This event – though seemingly a minor occurrence that largely escaped the attention of many analysts – reflects broader and more concerning trends (particularly for the West) emerging within the global uranium market, in which Kazakhstan plays a pivotal role.

Photo source: NAC Kazatomprom JSC

BACKGROUND: The strategic significance of uranium extends well beyond its military applications. The rapidly increasing global interest in nuclear energy—among both economically advanced and developing countries—is contributing to uranium’s emergence as a commodity of critical strategic value. According to estimates by the International Energy Agency (IEA), in addition to the existing 420 nuclear reactors worldwide, 63 new reactors are currently under construction, and the operational lifespan of a further 60 reactors is being extended. As a result, uranium's importance is projected to grow steadily in the years ahead. The present and future stability of the global nuclear energy sector is therefore highly contingent upon reliable access to substantial, readily extractable uranium reserves located in politically stable and predictable nations. It is precisely in this context, however, that significant challenges begin to surface.

Following the onset of Russia’s aggression against Ukraine in February 2022, Western access to two critical sources of both enriched and unenriched uranium has been partially obstructed. U.S. sanctions targeting Russian uranium have jeopardized U.S. access to this supply, while geopolitical instability—marked by a pronounced anti-Western orientation—in Sub-Saharan Africa, particularly in Niger, has effectively severed France’s access to locally sourced unenriched uranium. Exacerbating this situation, other major African uranium producers, including Namibia and Tanzania, are increasingly inclined to cooperate with Russia and China in uranium extraction activities. This emerging alignment places them in growing opposition to Western companies and their strategic interests.

At present, the already limited list of geopolitically stable, world-class uranium-producing nations has effectively narrowed to just three: Kazakhstan, Canada, and Australia. Among them, Kazakhstan stands as the global leader in the production of unenriched uranium, accounting for over 40 percent of total global output, and ranks as the second-largest country in terms of uranium reserves.

The primary concern lies in the fact that, despite its considerable wealth in natural resources, Kazakhstan is unable to fully leverage its vast resource potential. The country remains heavily dependent on two dominant geopolitical actors—Russia and China—both of which exert significant influence over the direction and development of Kazakhstan’s uranium-producing sector. Most critically, these two states maintain increasingly strained relations with the West.

Consequently, certain Kazakhstan-based analysts have voiced suspicions that the underlying cause of the operational halt at Inkai was pressure exerted by Russia, allegedly in response to Kazakhstan’s post-2022 efforts to alter the logistics of its uranium exports by decreasing reliance on Russian transit routes and instead utilizing the Trans-Caspian International Transport Route (commonly referred to as the Middle Corridor) as an alternative to exporting uranium through Russian territory.

IMPLICATIONS: The global uranium industry is currently characterized by rapidly increasing demand alongside growing uncertainty regarding the reliability of supply, driven largely by global and regional geopolitical disruptions. Within this context, Kazakhstan’s role as a resource-rich and historically stable supplier of uranium has acquired a qualitatively new significance. Notably, Kazakh authorities have publicly committed to boosting uranium production in 2025 and to diversifying both their export destinations and logistical routes, aiming to reduce the country's reliance on Russia. Nevertheless, the “Inkai incident”—which allegedly represents only the visible portion of deeper structural dynamics affecting Kazakhstan’s uranium sector—raises three key concerns.

First, can Kazakhstan successfully restructure its existing logistical routes and thereby reduce its strategic dependence on Russia? On the surface, such a shift appears feasible. According to statistics provided by Kazakh authorities, the country has made tangible progress in increasing uranium shipments through the Middle Corridor. Available data indicate that approximately 64 percent of West-bound uranium exports are now transported via this route. Moreover, Kazakhstan has also expanded its uranium exports to Western markets, with shipments destined for the United States gaining particular prominence.

The reality, however, appears significantly more complex. Despite recent efforts to diversify transit routes, a substantial portion of Kazakhstan’s uranium exports continues to be transported through Russian territory. Furthermore, Russia’s state-owned corporation Rosatom maintains (in)direct control over at least five of Kazakhstan’s fourteen major uranium production sites, reinforcing Russia’s strategic influence over the sector. In addition, the Middle Corridor presents notable challenges. Geopolitically, Georgia—an essential transit country along the route—occupies a critical position, and its political leadership has demonstrated increasing alignment with Moscow, potentially complicating matters should Russo-Western relations further deteriorate. From a logistical standpoint, representatives of the Canadian firm Cameco have expressed concerns, stating that the Middle Corridor “has proven to be neither reliable nor predictable,” due to the complex network of countries traversed and the numerous permits required for transit.

Compounding these challenges is the apparent ambivalence within Kazakhstan regarding the exclusion of Russia from its current uranium transportation framework. Specifically, Kazakh officials have indicated that the country does not intend to significantly expand the use of the Middle Corridor for uranium exports. Additionally, many Kazakhstan-based experts express skepticism about any prospective reduction in cooperation with Rosatom (i.e., Russia). On the contrary, a prevailing view among these analysts is that bilateral collaboration in the uranium sector is likely to deepen in the future.

Second, what is the actual role of China in Kazakhstan’s uranium industry and how will this role evolve? At present, China is the world’s second-largest consumer of uranium, following the United States, and its demand is expected to continue rising. Kazakhstan serves as China’s primary source of uranium: according to several studies, over half of Kazakhstan’s uranium output is currently exported to China, with some estimates suggesting this figure may be as high as 60 percent. This situation, as noted by representatives of major Western uranium-related enterprises, “raises concerns about reduced availability for Western markets, potentially exacerbating global supply constraints,” a challenge that is already beginning to manifest within the industry.

Rosatom-affiliated Uranium One Group recently concluded an agreement with the Chinese firm SNURDC Astana Mining Company Limited, a subsidiary of the State Nuclear Uranium Resources Development Co., Ltd. Under this arrangement, the Russian side transferred its shares in uranium-producing sites located in Northern Kazakhstan (Northern Khorasan) to its Chinese counterparts. At present, there is no consensus among experts regarding China’s rationale for acquiring stakes in what is considered a relatively depleted and comparatively minor uranium production site.

While some analysts contend that the acquisition primarily serves China’s geoeconomic objectives—particularly in light of projections indicating a substantial increase in the country’s uranium consumption over the coming years—others emphasize a more overtly geopolitical dimension to China’s actions. Notably, Stanislav Pritchin of the Central Asia Department at the Institute of World Economy and International Relations of the Russian Academy of Sciences has drawn attention to China’s established practice of acquiring “unpromising” oil and natural gas deposits. In his view, such acquisitions function as instruments for expanding China’s strategic presence within the host country.

Third, what is the future role of Western companies in Kazakhstan’s uranium industry? Given that neither China nor Russia appears willing to reduce their involvement in the sector—thereby sustaining Kazakhstan’s strategic dependency on both actors—serious concerns have emerged regarding the potential marginalization or even eventual withdrawal of Western firms from the country’s uranium landscape. Indeed, some Kazakhstan-based experts have implicitly acknowledged a widely discussed notion circulating in Western policy and business circles: the ongoing bifurcation of the global uranium industry. This refers to the emergence of a distinct segmentation of uranium supply chains along geopolitical lines, with one stream aligned with the West and the other with the China-led bloc. Within this context, it is feared that Kazakhstan may ultimately be compelled to align more closely with the latter and reduce its cooperation with Western partners accordingly.

Undoubtedly, such a scenario would only be likely to materialize in the event of a further deterioration in political and economic relations between China (and, under certain conditions, Russia) and their Western counterparts. While this scenario remains hypothetical at present, it is by no means implausible.

CONCLUSION: Although Kazakhstan and its political leadership have expressed strong interest in expanding foreign—particularly Western—participation in the country’s uranium industry, the influence of external geopolitical dynamics cannot be overlooked. As uranium increasingly assumes a role in the global energy mix comparable to that historically occupied by fossil fuels, the issue of access to and supply of this resource has transcended purely economic considerations and has firmly entered the realm of geopolitics.

In light of the intensifying geopolitical competition between East and West over access to emerging markets and spheres of influence, it is conceivable that China and its strategic partners may seek to curtail Western access to Kazakhstan-based uranium—mirroring developments in Sub-Saharan Africa, where Western firms are increasingly being displaced from uranium-related ventures. To avert a potential supply shock—akin to that experienced in the oil and natural gas sector following Russia’s attempt, in the aftermath of February 2022, to weaponize hydrocarbon exports as a means of exerting geopolitical pressure on the West—it is imperative that Western companies (and, arguably, governments) begin to explore alternative uranium sources to sustain their nuclear energy agendas. Given the small number of globally significant suppliers, increased attention should be directed toward Canada and Australia, which possess substantial uranium reserves and are regarded as geopolitically stable and reliable partners.

AUTHOR BIO: Dr. Sergey Sukhankin is a Senior Fellow at the Jamestown Foundation and the Saratoga Foundation (both Washington DC) and a Fellow at the North American and Arctic Defence and Security Network (Canada). He teaches international business at MacEwan School of Business (Edmonton, Canada). Currently he is a postdoctoral fellow at the Canadian Maritime Security Network (CMSN).

Feature Articles

|

Earlier Articles

|

|

Forums and Events |

Latest From the Turkey Analyst

|

Hot Topics

|

Most read this month

|

![]()

Silk Road Paper S. Frederick Starr, Greater Central Asia as A Component of U.S. Global Strategy, October 2024.

Silk Road Paper S. Frederick Starr, Greater Central Asia as A Component of U.S. Global Strategy, October 2024.

Analysis Laura Linderman, "Rising Stakes in Tbilisi as Elections Approach," Civil Georgia, September 7, 2024.

Analysis Mamuka Tsereteli, "U.S. Black Sea Strategy: The Georgian Connection", CEPA, February 9, 2024.

Silk Road Paper Svante E. Cornell, ed., Türkiye's Return to Central Asia and the Caucasus, July 2024.

Book Svante E. Cornell, ed., "The Changing Geopolitics of Central Asia and the Caucasus" AFPC Press/Armin LEar, 2023.

Book Svante E. Cornell, ed., "The Changing Geopolitics of Central Asia and the Caucasus" AFPC Press/Armin LEar, 2023.

Silk Road Paper Svante E. Cornell and S. Frederick Starr, Stepping up to the “Agency Challenge”: Central Asian Diplomacy in a Time of Troubles, July 2023.

Silk Road Paper S. Frederick Starr, U.S. Policy in Central Asia through Central Asian Eyes, May 2023.

The Central Asia-Caucasus Analyst is a biweekly publication of the Central Asia-Caucasus Institute & Silk Road Studies Program, a Joint Transatlantic Research and Policy Center affiliated with the American Foreign Policy Council, Washington DC., and the Institute for Security and Development Policy, Stockholm. For 15 years, the Analyst has brought cutting edge analysis of the region geared toward a practitioner audience.

Sign up for upcoming events, latest news and articles from the CACI Analyst